Ten waypoints for CSRD – Double Materiality

The double materiality analysis plays a key role in the Corporate Sustainability Reporting Directive (CSRD). This gives users of annual reports insight into the impact, opportunities and risks in the field of sustainability and can provide input for the strategic direction of a company. Our message is clear: despite the challenges, it is possible to report on this transparently. This is also evident from the good practices that we are already encountering in the market.

In short

• Double materiality analysis plays a key role in CSRD; it provides input towards a company’s sustainable and financial direction

• AFM has assessed the application of double materiality analyses in 2023 annual reporting

• 10 waypoints provide support to companies in preparing the double materiality analysis

• Supervision on application of CSRD begins with 2024 annual reporting

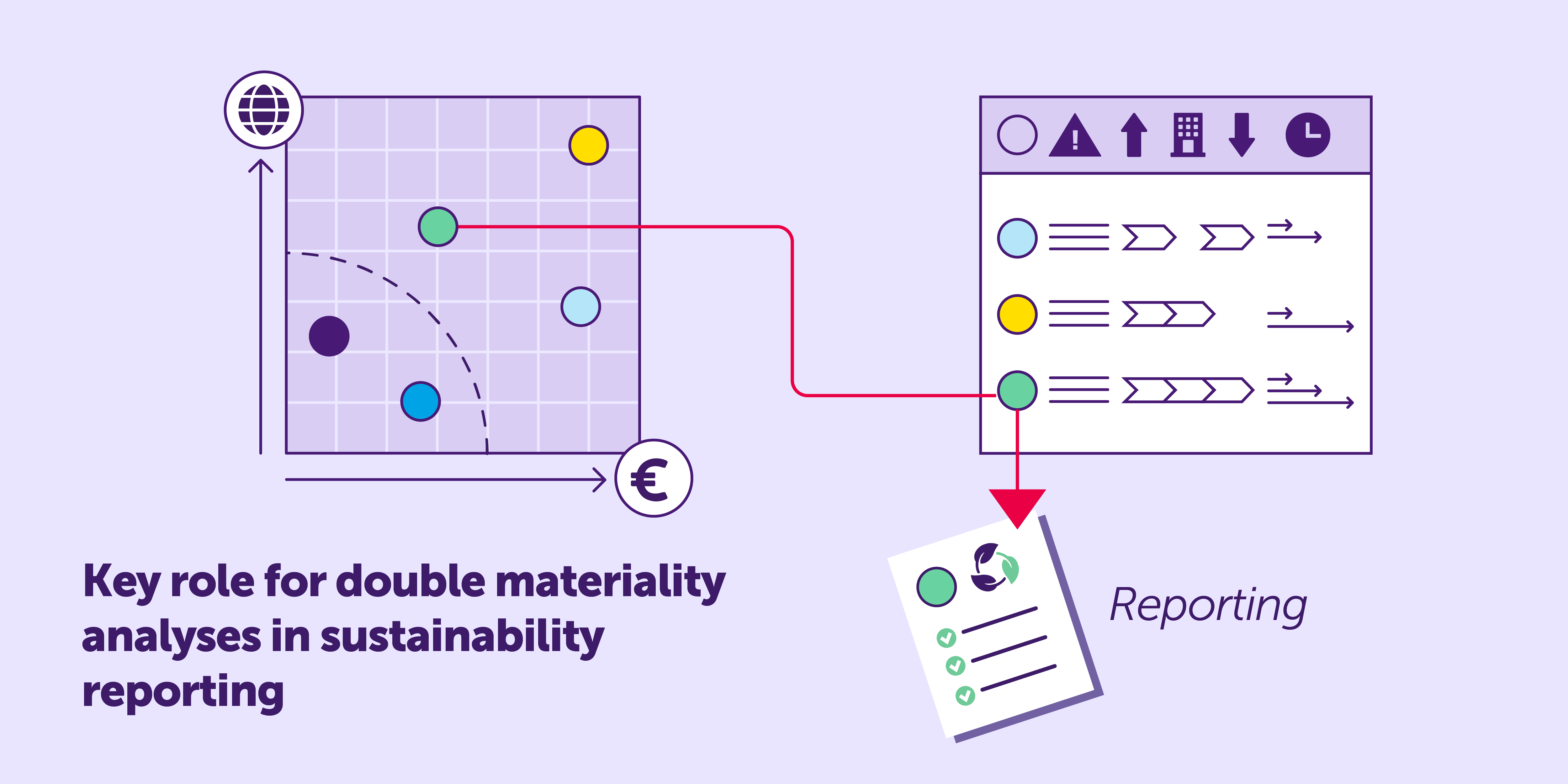

Double materiality analysis plays a key role in CSRD

The CSRD will come into effect for large listed companies as from the 2024 financial year. The double materiality analysis plays a key role in this. This analysis makes it clear what effect a company has on the outside world (impact materiality) and how sustainability matters can have an effect on the wellbeing of a company (financial materiality). Information is material when its omission or misrepresentation could influence the decision-making of the user of the sustainability information.Hanzo van Beusekom, AFM board member: 'Comprehensible and transparent communication on double materiality is important, because this is the cornerstone for proper sustainability reporting. Our review shows that it can be done! Our research has delivered 10 waypoints that anyone can benefit from either when conducting or using the double materiality analysis.'

Click for download of a Hi-res version

Text in infographic

The infographic shows a circular flowchart that guides users from Stakeholder engagement, where interests and views are collected, to Due diligence, to developing the Double materiality analysis to Reporting, which in turn can lead to new input for discussions with stakeholders.

10 Waypoints for CSRD – double materiality

Stakeholder engagement: show the manner in which stakeholders are engaged1. Be transparent on the representativeness of stakeholder engagement.

2. Disclose inputs received from stakeholders.

Due diligence: identify the sustainability matters

3. Use due diligence to identify sustainability matters.

4. Use international frameworks, such as the OECD Guidelines.

5. Disclose the relationship between due diligence and the double materiality analysis.

Double materiality analysis: disclose the analysis in a transparent manner

6. Disclose the role of the value chain.

7. Connect the business activities to identified material topics.

8. Provide insight into the materiality assessment of sustainability topics.

9. Disclose the materiality of impacts, risks and opportunities.

10. Report on the relationship between impact and risk in the short and long term.

AFM has assessed the application of double materiality analyses in 2023 annual reporting

To gain insight into how listed companies already provide disclosures on important themes in the double materiality analyzes in their annual reporting for 2023, the AFM conducted research into 29 companies. AFM found that companies find the new requirements complex, and that they have already started making the necessary adjustments in 2023. Many of these companies report that their implementation processes are still ongoing.10 waypoints provide support in preparing a double materiality analysis

Based on this research, the AFM provides 10 waypoints that can support companies in implementing the double materiality analysis in their reporting. These waypoints are based on the European Sustainability Reporting Standards (ESRS) and a number of good practices that we already see in annual reporting from listed companies. This also supports users in entering into a conversation with the company about its direction.Supervision on compliance with CSRD begins with 2024 annual reporting

In our supervision on annual reporting for the 2024 financial year, we assess how companies deal with the CSRD requirements. We do this through our regular desktop reviews. In addition, we will conduct thematic research into a sustainability theme related to CSRD compliance.Tags

Audit firmsContact for this article

+31 6 31 77 76 86

Would you like to receive the latest news from AFM?

Subscribe to our newsletter, we will keep you up-to-date.